Like global markets, Australia’s interest rates hover at record lows (RBA Cash rate is 0.25% and 10 year bond yield is ~0.9%) whilst the equity market has increased strongly from the March lows … the S&P/ASX 200 is up 36% from its March low around 4,400 to its latest level around 6,000.

PANDEMIC

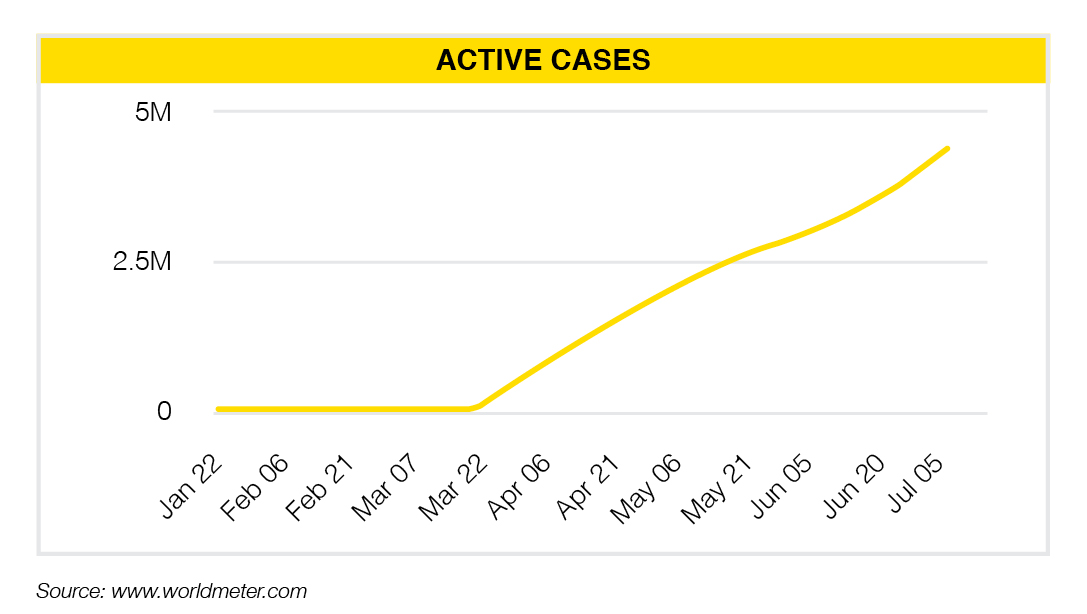

- A second acceleration of global cases has threatened many economies around the world who opened their economies and relaxed restrictions. Most notable accelerations are in the large population countries that include USA (~3million cases), and major emerging economies Brazil (~1.7million cases), India (~0.7m cases) and Peru (~0.3m cases).

- The chart below shows the global COVID-19 curve is not flattening but is reaccelerating and, whilst still early days, there are no short-term signs of successful vaccines or treatment.

GEOPOLITICAL

- China appears to have taken advantage of the focus on COVID-19 and appears focused on strengthening their position around South East Asia with a stronger hold on Hong Kong, small border conflicts with India and the Tibetan Plateau, as well as their land claims in the east China Seas.

o The Uhe USA continues its drive to reduce its dependence on China for technology supply chains and is requesting companies to shift their manufacturing away from China. - Whilst Donald Trump has always been anti-globalisation it appears COVID-19 and its rapid international spread has increased the speed away from globalisation and is now a very strong reality as borders remain closed and international travel is subdued for many months to come.

o It is worth noting, there are reports of an increased trade war between the US and EU with many expectations of increased trade tariffs before the end of the year.

GLOBAL ECONOMY

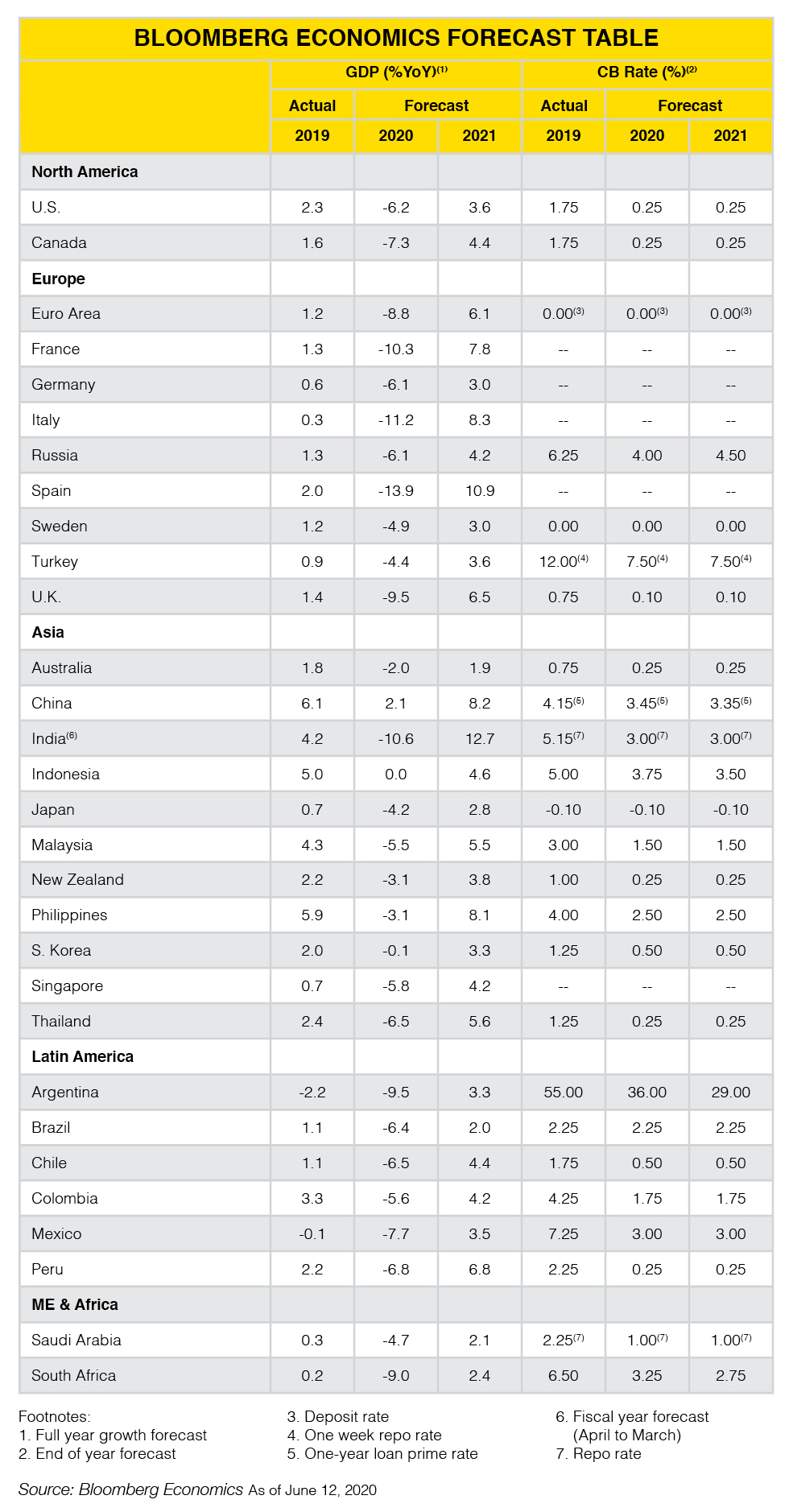

- Whilst the global economy is currently in recession the question everyone is looking to answer is how quickly the recovery will be. Hopes for a V-shaped recovery appear dashed with the second acceleration of COVID-19, so 2020 GDP change will be a deep contraction with strong headline growth numbers in 2021 that may fall short of returning to 2019 GDP.

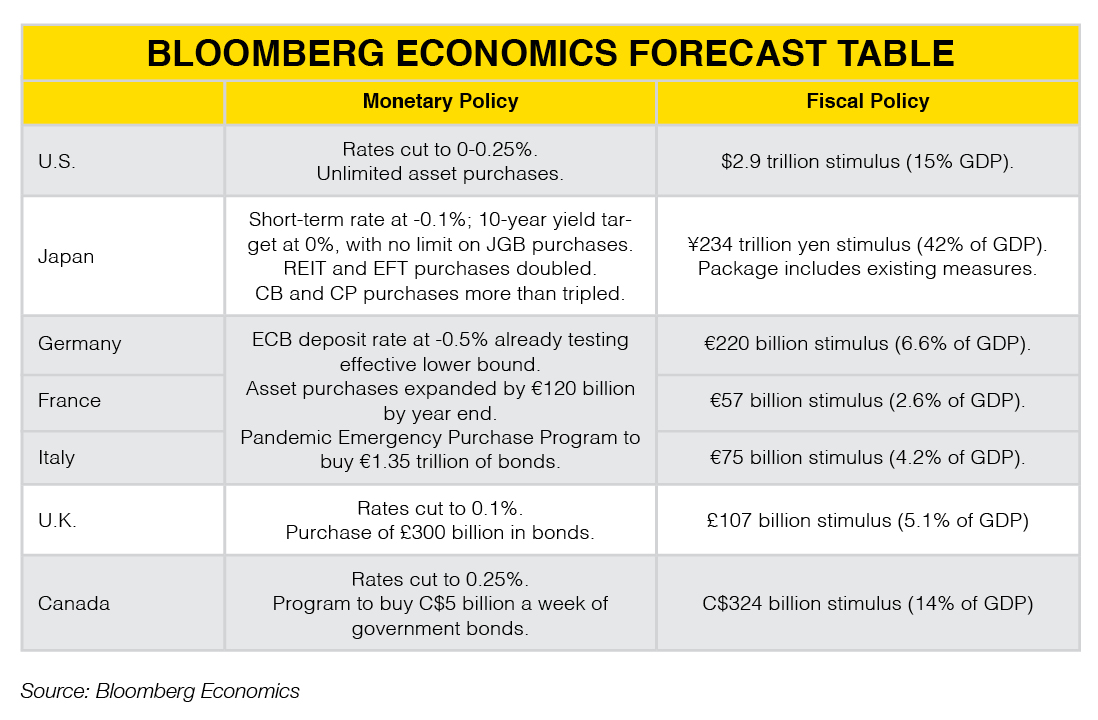

- The current recession is accompanied by government enforced high unemployment that most economists believe will remain elevated for years to come… this may keep inflation down, despite the enormous global fiscal and monetary stimulus provided from all major economies (see second below).

GLOBAL MARKETS

- The second quarter returns from all risky asset classes has been almost as strong as the collapse that occurred over February and March. Despite the deep recession and weak economic outlook, equity markets have gone from strength to strength with valuations at multi-year record highs across numerous markets including the biggest of them all, USA.

- Interest rates remain around 0% or lower around the world and credit spreads have narrowed, in line with equity markets providing strong short term returns and high valuations.

- Whilst economic growth forecasts are being lowered and company earnings guidance has diminished, markets are strong simply because they have confidence the central banks or government fiscal stimulus will bail them out. Printing money has become the norm when market liquidity starts to dry up so markets are up but are they complacent?

- Either way, despite the central bank and fiscal support, this all adds up to low future returns for all asset classes.

GLOBAL RISKS

- The primary risk continues to be the global recovery to COVID-19 and the desperate need for a vaccine or successful treatment. Whilst this appears to be many months or even years away, any positive news in this regard will translate into rapid change across markets, economies and general human behaviour.

o Given end of year reporting is soon to start, all eyes will be on company earnings to finally see how bad the damage is… this could result in high market volatility if reporting starts out worse than expected. - Secondary risks are focused on trade wars between US, China, and EU.

AUSTRALIAN ECONOMY

- Australia is currently in its first recession since 1991… this will be confirmed as a technical recession when the June quarter’s economic growth figures are reported as negative… but this won’t occur until early September. The March quarter GDP results were only a decline of 0.3% but June is expected to be significantly lower.

- Unemployment has increased from 5.1% in February to the latest level of 7.1% in May… whilst this appears to be a small increase compared to other nations, Australia’s participation rate has declined from 65.9% in February to its May level of 62.9% which is an additional 3%… meaning Australia’s true unemployment rate is over 10% and it would be much higher if it wasn’t for the government’s JobKeeper.

AUSTRALIAN MARKETS

- Like global markets, Australia’s interest rates hover at record lows (RBA Cash rate is 0.25% and 10 year bond yield is ~0.9%) whilst the equity market has increased strongly from the March lows … the S&P/ASX 200 is up 36% from its March low around 4,400 to its latest level around 6,000.

- The Australian dollar has followed risky markets upwards and currently trades just short of $0.70USD.

- Reporting season starts towards the end of July and is likely to create volatility assuming all things equal between now (6 July) and then.

AUSTRALIAN RISKS

- In addition to COVID-19, Australia’s relationship with China is currently strained after Australia supported calls for an inquiry into China’s handling of COVID-19. China has placed trade tariffs on several Australian goods including Barley; Australia has responded with accusations of cyber-spying and the government recently announced a $250billion defence spend designed to beef up Australia’s military power including the purchase of long-range missiles.

- Victoria is currently experiencing a second acceleration of new COVID-19 cases and this has resulted in a partial lockdown in Melbourne and state borders closing to Victorians … this risk example could easily appear in other Australian jurisdictions and slow down Australia’s COVID-19 recovery; which so far has been amongst the fastest in the world.

ASSET ALLOCATION SUMMARY

- Bond yields are low, equity markets appear expensive thanks to global government stimulus, and real assets are suffering from the global recession significantly reducing rents.

- Valuations present little buying opportunities although the one stand-out appears to be providers of liquidity… for example, cashed up private equity although there are few that are accessible.

- Whilst equity risk premiums had expanded into March creating some buying opportunities, they have once again reduced resulting in low future expected returns of all diversified portfolios, whether conservative or aggressive or in-between. Likely returns are probably low to mid-single digit returns over the next 5 plus years.

- Equity markets are still priced and expected to outperform the less risky credit and bond markets over the long term (i.e. 5 to 10 years) but volatility is likely as reporting season approaches, meaning increasing portfolios towards risky assets must be prepared to accept this greater volatility and further downside risk.

- With Cash interest rates only marginally lower than Bond Yields, it appears Cash’s liquidity is attractive and it may be appropriate to hold surplus funds in cash in case of market further market declines or even to cushion economic losses, given equity market valuations don’t appear to match the economic stress before them

- Regular rebalancing of asset classes is generally recommended but care must be taken as transaction costs are significantly higher than they were last quarter.

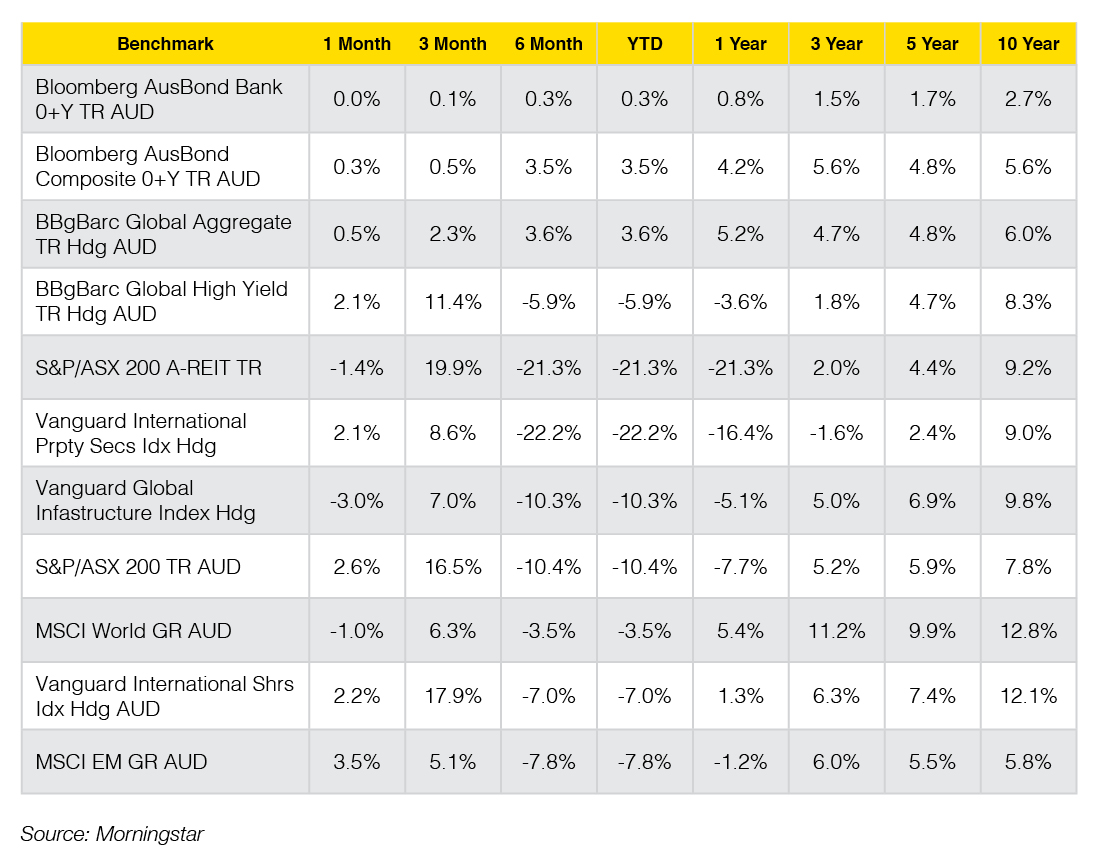

ASSET ALLOCATION SUMMARY (TO 30 JUNE 2020)

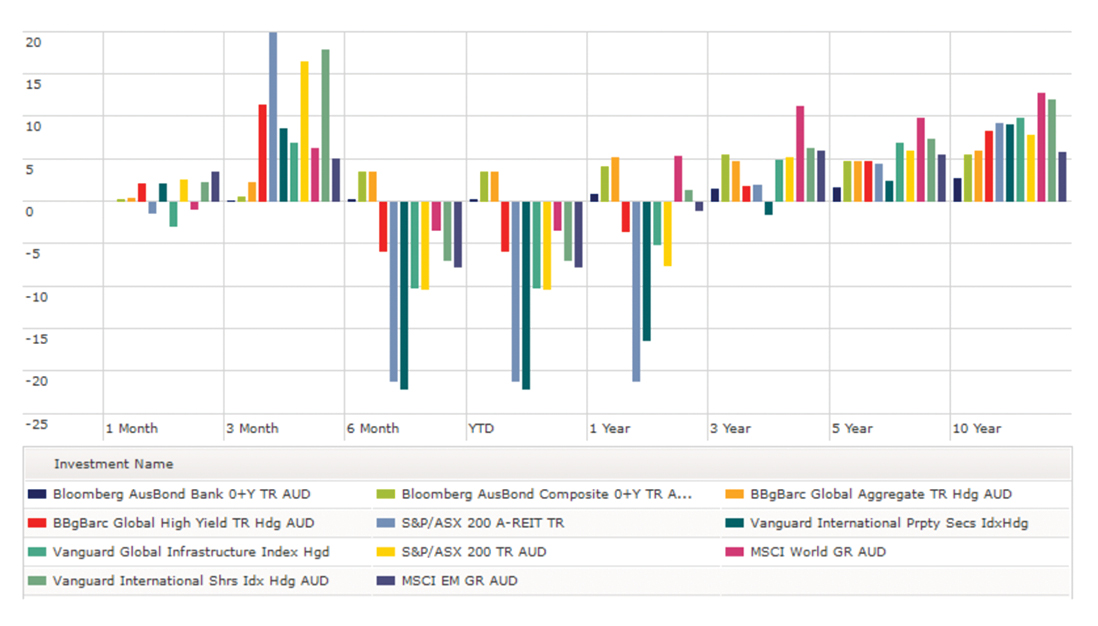

- Real Assets have performed the worst in 2020 as the global economy shuts down and a high proportion of the population avoids the workplace and stays home.

- After a poor first quarter, equities have bounced back strongly and the 2nd quarter say greater than 15% returns from Australian equities (16.5%), Australian REITs (19.9%), and Hedged Global Equities (17.9%).

The last month has been a little more volatile and with mixed results as coronavirus commences a second acceleration of cases.

Latest News Articles

Back to Latest News

20 January 2026

What a Financial Plan Actually Looks Like

If you’ve ever found yourself asking “what is a financial plan?” and immediately felt overwhelmed, you’re not alone. For many Australians in their 20s,...

20 January 2026

Realistic Budgeting Tips for Australians in 2026

Who doesn’t love some easy budgeting tips? If you’ve noticed your money disappearing faster than it used to, you’re not alone. Between housing costs,...

20 January 2026

Economic Snapshot – December 2025 Update

This article was prepared by Michael Furey, Principal of Delta Research & Advisory, on behalf of HPartners Group. DECEMBER 2025 IN SUMMARY Strong and...