Economic Snapshot – April 2026

The Iran War continues, although appears to be all but lost for the USA, as Iran clearly now controls the global energy supply via the Hormuz Strait.

This April economic shapshot article is prepared by Michael Furey, Principal of Delta Research & Advisory, on behalf of the HPartners Group.

Summary

- April provided a bounce back in most sharemarkets and particularly the USA as the S&P500 returned over 10% in US Dollar terms. In, unhedged Australian dollar terms, the US Dollar weakness (AUD is now over $0.72USD), reduced that to over 5%; still high for just one month.

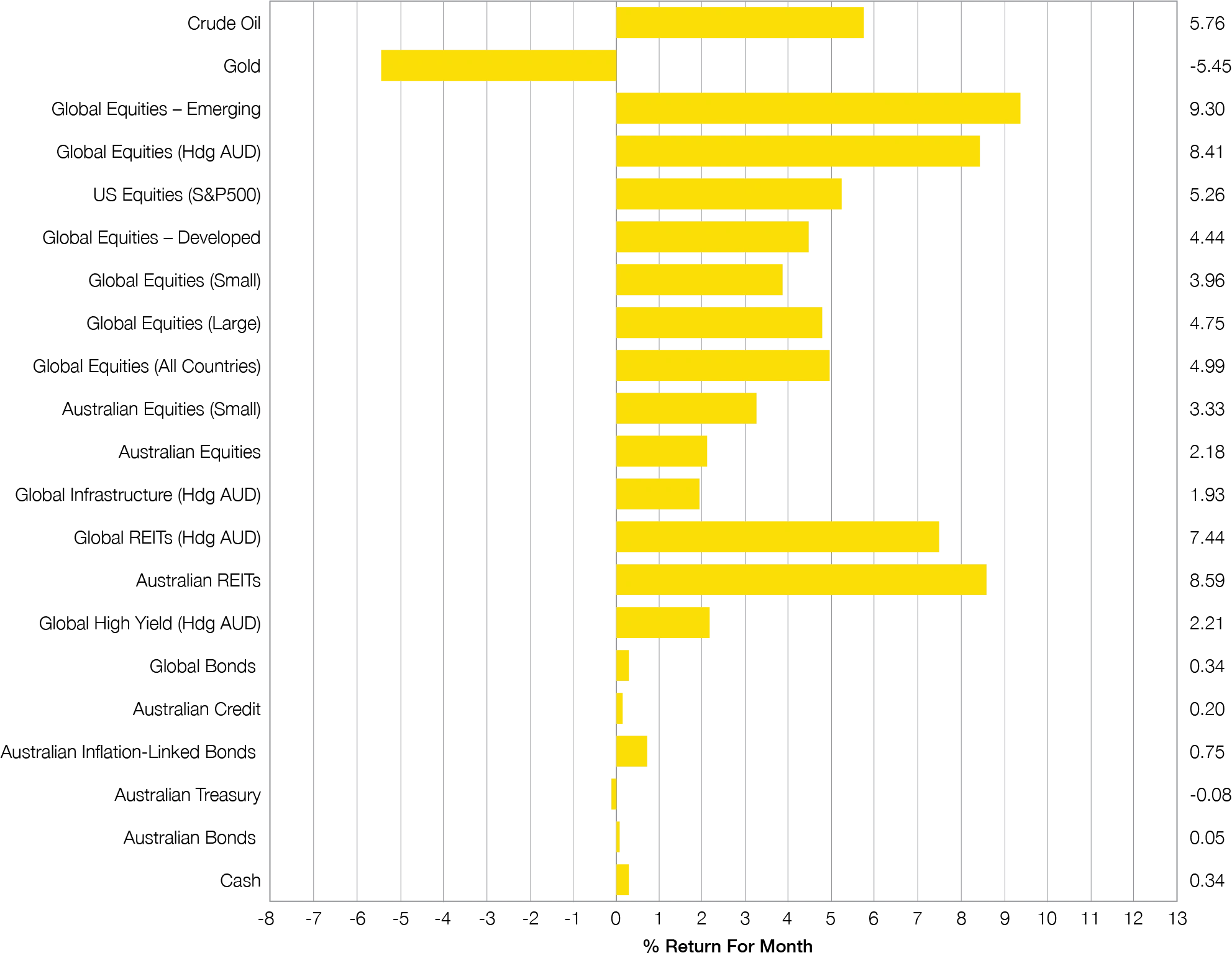

- As Chart 1 below shows, only Gold and the slightly higher yielding Australian Treasury Bonds produced a negative return for April with all sharemarket asset classes returning around 2% or more. In Australian dollar terms, the best return came from Emerging Markets followed by the recently beaten up, Australian Property (REIT) market.

- The Iran War continues, although appears to be all but lost for the USA, as Iran clearly now controls the global energy supply via the Hormuz Strait. The higher energy prices are expected to sustain for the remainder of 2026 feeding into higher inflation for Australia and the rest of the world. This higher inflation does not guarantee future higher cash rates or lower bond returns for all, but the RBA appears concerned about pre-existing higher inflation which is why it has increased cash rates 3 times already in 2026. Markets are pricing up to 2 more rises.

- Our core investment message remains despite persistent downside risks from high sharemarket valuation in USA and the energy crisis. This means disciplined risk management rather than aggressive positioning changes. Shares continue to offer an attractive risk premium in specific markets, as do conservative bonds, but returns may be challenged from occasional short term volatility. Avoiding panic (selling) decisions continues to be a crucial investment issue today for long-term investors.

Chart 1

Risk on strongly assuming Hormuz operating normally

What Happened Last Month?

Markets & Economy

- After a rough start to 2026 for sharemarkets, they bounced back very strongly and particularly in the USA, where the S&P500 reached record highs after returning more than 10% in April (in USD). The main driver appeared to be renewed confidence in Artificial Intelligence stocks and a belief that the Iran War was over, but record high US sharemarkets is still very surprising to most.

- Coinciding with the sharemarket strength was US Dollar weakness. This is somewhat normal as the US Dollar typically weakens when sharemarkets are strong and strengthens when sharemarkets are weak. At the time of writing the Australian dollar is close to its long term average of $0.75USD, and is trading around $0.72USD.

- The Australian sharemarket was also positive in April but the 2% increase was relatively subdued as some of the largest stocks in the ASX, like CSL, Westpac, NAB, and Woodside, declined in value.

- Inflation figures in Australia continued to be higher than preferred by the RBA and they increased their cash rate for the 3rd time in 2026. As expected inflation is increasing across all major economies.

- At this stage, unemployment appears relatively healthy in Australia and around the world and appears to be one of the inflation drivers in Australia adding to the RBA’s challenges. Looking ahead, the unemployment will be a key indicator determining economic strength and potential interest rate movements.

Outlook

- High inflation results have started to flow through major economies of the world and so far, only Australia has increased its interest rates as our inflation rate was already high and not completely due to high energy prices.

- The big question now is how big an effect will the high energy prices have on the global and local economy. Most major economic agencies are not currently predicting recession, but they are downgrading their previous forecasts.

- Our current beliefs are that new investors should dollar cost average into sharemarkets and long-term investors should stay invested for the long-term.

- We believe portfolios should be underweight USA shares and high yield (junk) bonds due to near record high valuations. Markets continue to price in higher cash rates for Australia (~4.75% by the end of 2026), but conservative bond portfolios both global and in Australia, are providing strong expected returns over 5%pa.

- Diversification continues to be essential. Maintaining a balance between domestic and global exposures remains a prudent approach as 2026 unfolds. Rebalancing as pricing opportunities arise also continues to be appropriate for established portfolios.

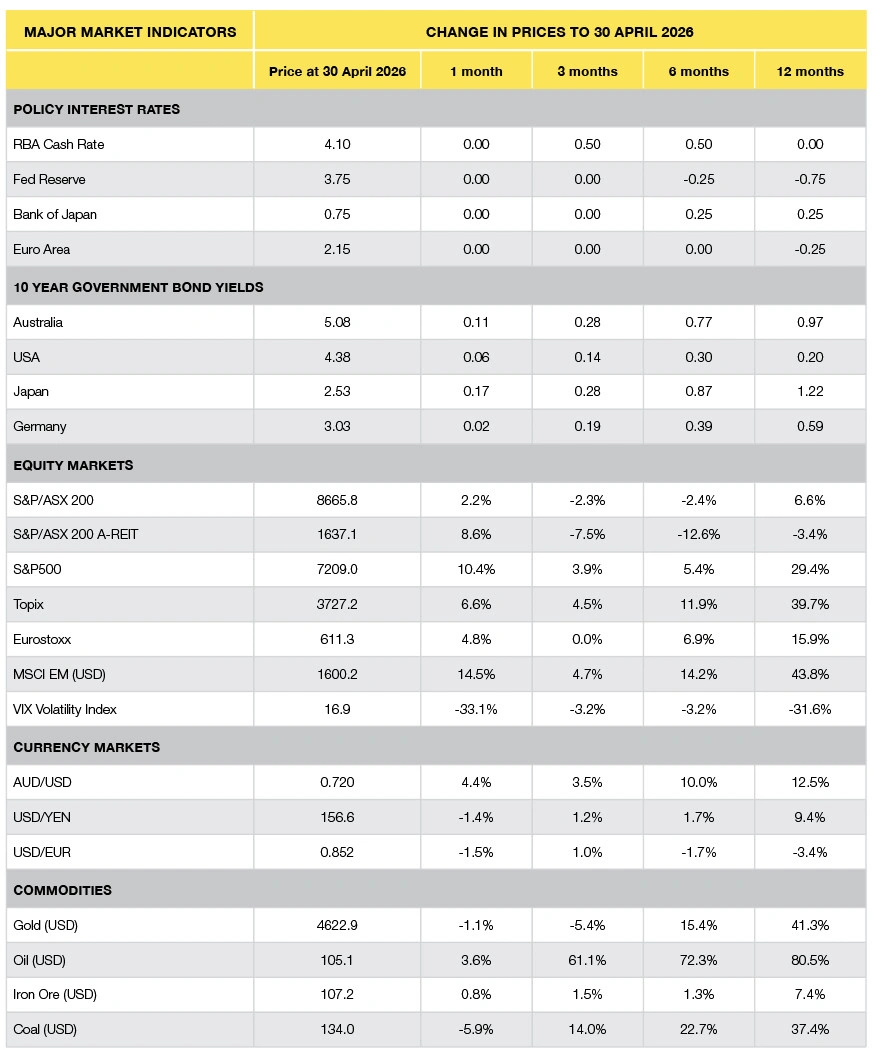

Major Market Indicators

Source: Morningstar, Trading Economics, Reserve Bank of Australia

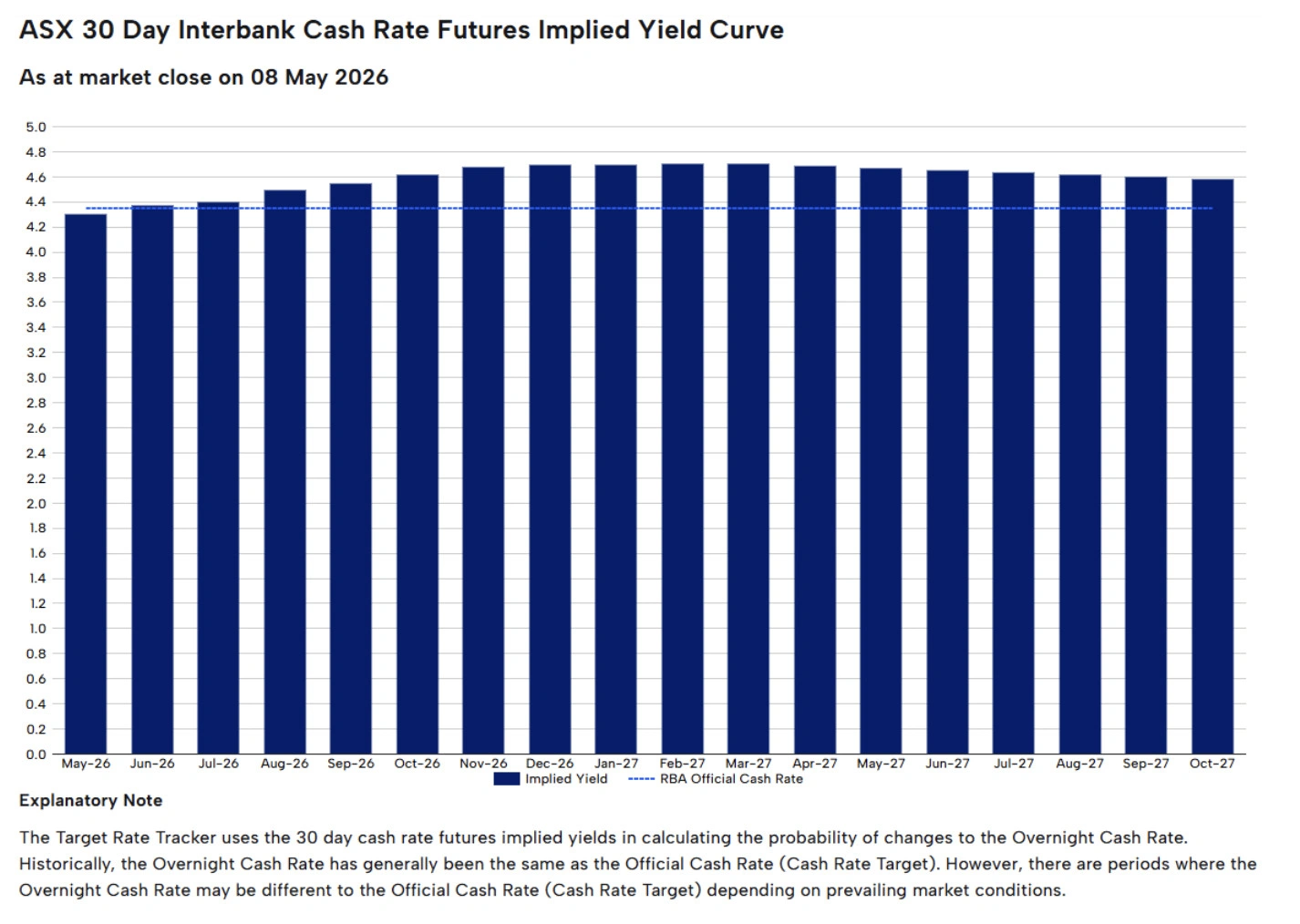

Market Expectations of Future RBA Cash Rates

The RBA hiked early May as previously predicted and still has another 1-2 hikes priced in for 2026:

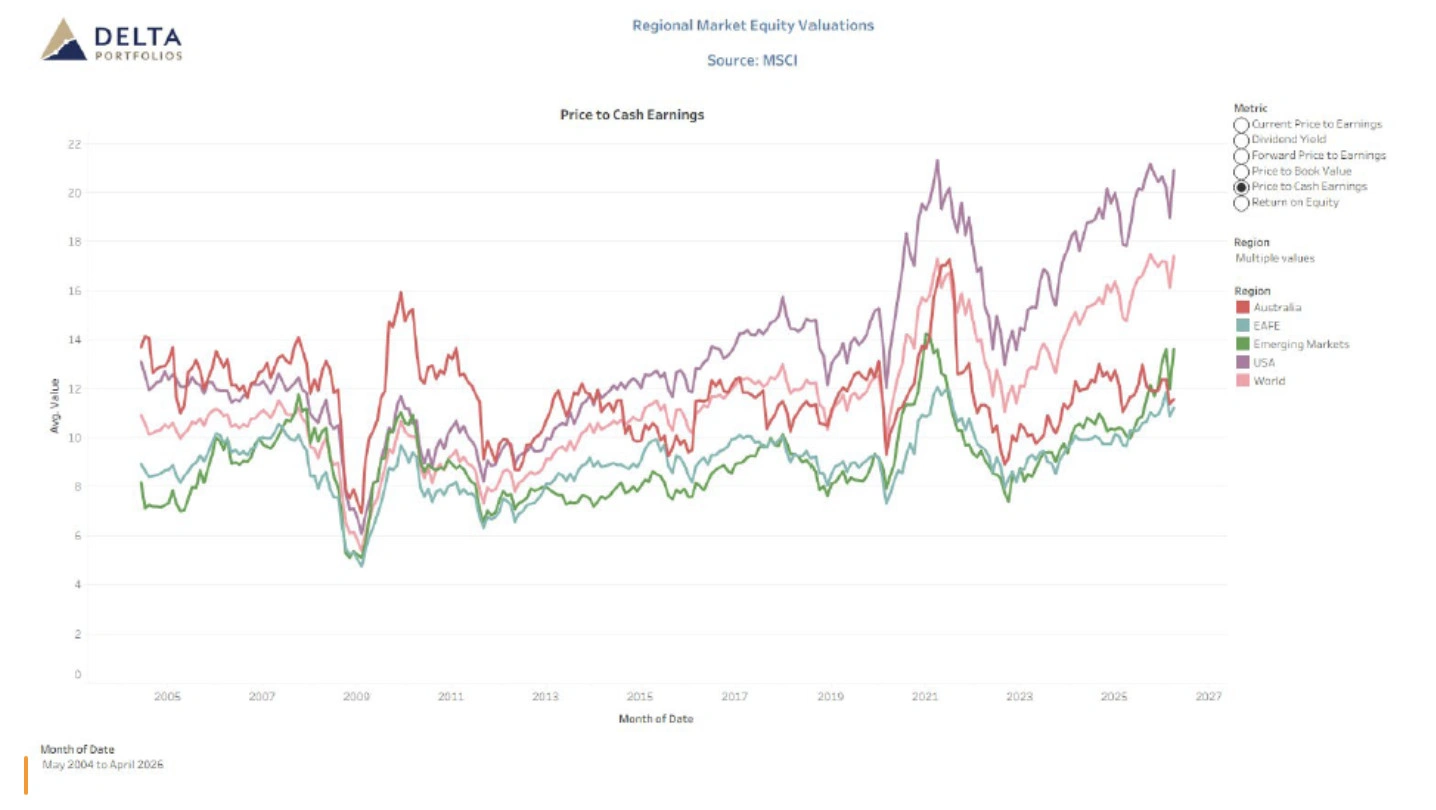

USA quickly back near its record high valuation… whilst Australia struggles

Published:

Share

Resources

A wealth of knowledge

Latest News

-

Financial Planner vs Accountant: Who Helps With What?

July 21, 2026

July 21, 2026

-

Where Is My Money Going? How to Track Spending In 5 Steps

July 14, 2026

-

Economic Snapshot – June 2026

July 14, 2026

-

Brisbane Property Market: Why Prices Are Holding Firm

July 7, 2026

-

Splitting Super in a Divorce: What Happens to Your Money?

July 7, 2026

-

Salary Sacrifice 101: Super Support to Boost Your Balance

June 30, 2026

Tools & Guides

Useful tools & guides to get you started

Video Guides

Useful videos to get you started

Financial Calculators

See what impact little changes can have