Economic Snapshot – February 2026

Diversification continues to be essential. Maintaining a balance between domestic and global exposures remains a prudent approach as 2026 unfolds.

This economic shapshot article is prepared by Michael Furey, Principal of Delta Research & Advisory, on behalf of the HPartners Group.

Summary

- February was a mixed month for investment markets with the best returns coming from Global Real Assets, including Global Property, Infrastructure, Gold, and Australian shares (a commodity exporting market). Weakest performance came from Australian Property as the higher inflation and cash rate increase by the RBA increased debt costs. US sharemarkets were also weak in Australian dollar terms as the US Dollar continued to weaken against the Aussie. This weakness included a sell-off in many tech stocks as investors shifted towards more defensive positions including cheaper value stocks.

- The US economy has numerous uncertainties thanks to the Iran War, and it’s almost forgotten that the Supreme Court finally ruled many of Trump’s tariffs illegal. Trump has responded by implementing 10% tariffs using a different law but without Congress approval this strategy, which is economically weak and unpopular, will hopefully disappear later this year after the latest batch expires in 150 days.

- Our core investment message remains despite persistent tail risks from high sharemarket valuation in USA and the current war(s). This means disciplined risk management rather than aggressive positioning changes. Shares continue to offer an attractive risk premium in specific markets, as do conservative bonds, but returns may be challenged from short term volatility. Avoiding panic (selling) decisions is a crucial investment issue today

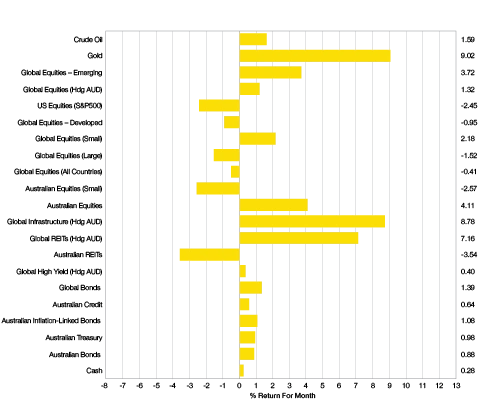

Chart 1

Good returns for Global Real Assets (& Aust Shares)

What Happened Last Month?

Markets & Economy

- USA showed continued disinflation with headline and core CPI around 2.5%. This resulted in a reduction in short-term inflation expectations whilst longer-term inflation expectations remained stubbornly high.

- The US Federal Reserve Bank kept its cash rates steady and suggested rates may stay higher for longer, but at the time of writing that is changing as high oil prices serves as a tax on the economy suggesting rates may start to now come down faster than previously expected as the economic outlook weakens

- Only Australia’s central bank, Reserve Bank of Australia, changed interest rates in 2026 with a 25bps increase to 3.85% as inflation remains above their target range (3.8% vs 2%-3%). The European Central Bank and Bank of Japan kept rates steady.

- As Chart 1 shows, major asset class returns were mixed in February with the strongest coming from global real assets, Global Property (REITs), Global Infrastructure, Gold, and Australian Equities (a seller of commodities). Weakest returns, came from another real asset, Australian REITs, but this was mostly due to the increase in cash rates by the RBA. Australian Small Companies, and US equities, were also down with the latter weak due to a declining US Dollar against the Aussie.

- Bond markets all produced returns around 1% in February which is a strong result. High Yield the weakest as these risky assets declined in price a little due to some private credit defaults in the USA.

Outlook

- Whilst this update is supposed to be about February, it’s safe to say February seems like a long time ago as the Iran War is top of everyone’s mind. Oil prices have climbed over 40% and volatility has been high across all markets whether sharemarkets, commodity markets or bond markets.

- A persistent war is rarely good for affected economies and in this case the impact comes from high oil prices which serve like a tax on everyone – businesses, households, and governments. Whilst many believe the current war will be a relatively short one, the volatility is present and may continue for a little while and inflation may also produce a short term spike.

- If the war persists, to combat higher oil prices, central banks may change direction from inflation concerns where they would increase cash rates, to economic concerns, where they might decrease cash rates. This is not the case in Australia yet, as expectations have shifted to continued higher cash rates. However, in the USA there currently appears little sign of a change and in Europe and Japan.

- For now, sharemarkets are likely to be volatile as different markets navigate their different energy supply needs. Either way, sticking to the long-term plan is essential and panicking by selling to time markets should be avoided.

- Diversification continues to be essential. Maintaining a balance between domestic and global exposures remains a prudent approach as 2026 unfolds. Entering new investment positions are best approached using a dollar-cost averaging approach and rebalancing as pricing opportunities arise continues to be appropriate for established portfolios.

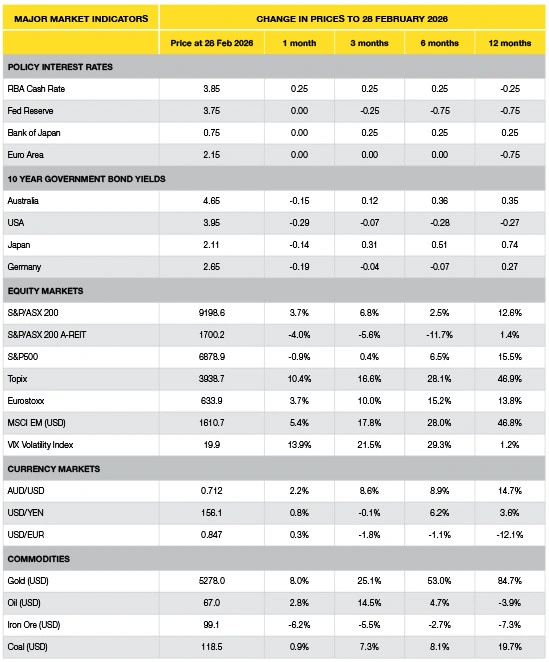

Major Market Indicators

Source: Morningstar, Trading Economics, Reserve Bank of Australia

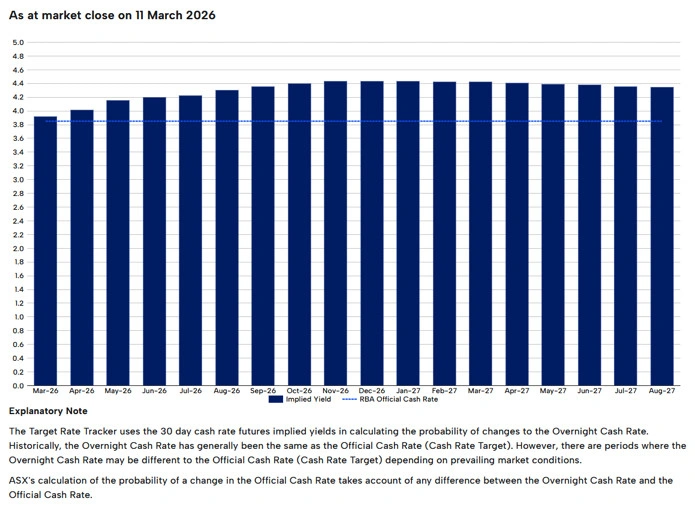

Market Expectations of Future RBA Cash Rates

Expectations have increased 20bps to be 4.45% cash rate by end of 2026

US Growth Valuation correcting whilst cheaper Value markets improve

Published:

Share

Resources

A wealth of knowledge

Latest News

-

Age Pension Assets Test 2026: How Much Can You Have?

July 28, 2026

July 28, 2026

-

Trump Tariffs Australia: What It Means for Your Money

July 28, 2026

-

Financial Planner vs Accountant: Who Helps With What?

July 21, 2026

-

Where Is My Money Going? How to Track Spending In 5 Steps

July 14, 2026

-

Economic Snapshot – June 2026

July 14, 2026

-

Brisbane Property Market: Why Prices Are Holding Firm

July 7, 2026

Tools & Guides

Useful tools & guides to get you started

Video Guides

Useful videos to get you started

Financial Calculators

See what impact little changes can have