Economic Snapshot – January 2026

Prepared by Michael Furey

This article is prepared by Michael Furey, Principal of Delta Research & Advisory, on behalf of the HPartners Group.

Summary

- Economic and investment conditions remained broadly constructive in January. The month was characterized by moderating inflation, resilient labour markets, and decent corporate earnings. However, these were offset by continuing geopolitical and policy uncertainty. This uncertainty led to a much weaker US Dollar which declined against all currencies including the Australian dollar.

- Risky assets generally delivered positive returns to start 2026. Notably, market leadership has begun to broaden beyond the narrow “mega-cap” cohort that drove markets for much of the prior two years, with Emerging Markets significantly outperforming their developed peers.

- Global growth expectations for 2026 have been revised slightly higher (now a little above 3%) as disinflation progresses and financial conditions ease modestly. However, forecasters continue to flag elevated uncertainty around public debt levels and the durability of the disinflation trend.

- Unfortunately, in Australia, the story is more inflationary resulting in higher cash rates generally expected by the market for 2026.

- Our core investment message remains characterized by a delicate balance between improving economics but persistent tail risks from high sharemarket valuation in USA. This means disciplined risk management rather than aggressive positioning changes. Equities continue to offer an attractive risk premium in specific markets.

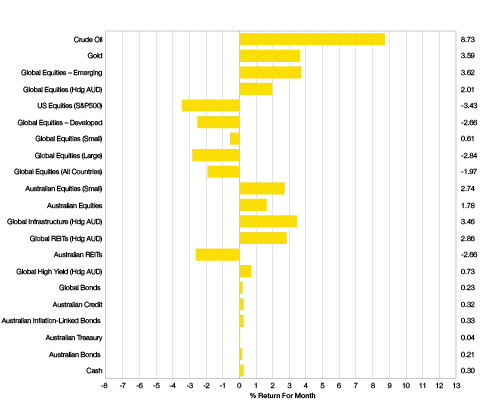

Chart 1

A slight comeback for Australian assets

What Happened Last Month?

Markets & Economy

- Global equity markets delivered a positive start to the year, with broad indices recording modest gains. In a shift from recent trends, Emerging Markets significantly outperformed developed peers.

- Within developed markets, the United States underperformed the rest of the world but still posted a small positive return. European and Asia-Pacific markets generally fared better over the month.

- Best performing stocks continued to broaden beyond the largest US technology names. Cyclical and value exposures, small companies, and several commodity-linked sectors outperformed in January.

- Overseas fixed income markets also advanced as investors weighed the prospect of eventual policy easing against still elevated but declining inflation. Credit spreads tightened on improving risk sentiment, supporting returns across investment-grade and high-yield segments.

- Australian equities outpaced some offshore benchmarks, with the ASX 200 delivering a solid gain for the month. Best performance came from resources and financials, while local bond markets reflected shifting expectations around the timing of any Reserve Bank policy moves and higher inflation in Australian dampened local fixed interest returns.

Outlook

- Headline inflation across most major economies (ex-Australia) continued to drift lower through late 2025, and projections released in January reinforced expectations of further progress toward lower central bank inflation targets. While underlying inflation remains above target in many jurisdictions, the breadth of extreme price pressures has narrowed.

- Central banks have largely moved from an aggressive tightening stance (i.e. higher rates) to a more data-dependent pause. Markets are now debating the timing and extent of the first easing steps, interpreting incoming data as consistent with a “higher-for-longer, but not higher-again” policy profile.

- In Australia, the Reserve Bank remains cautious due to still-elevated core inflation and pockets of labour-market tightness. Forward guidance no longer acknowledges the next move as down, as inflation data was higher than desired.

- Domestic data paints a picture of a slowing but still expanding Australian economy. Real GDP growth is running modestly below the longer term trend, supported by public investment and population gains. Labour market indicators showed some softening, yet unemployment remains low by historical standards.

- For Australian-based portfolios, diversification continues to be essential. Maintaining a balance between domestic and global exposures—with an eye to currency risk (in the face of a weakening US Dollar) and differing monetary policy trajectories—remains a prudent approach as 2026 unfolds.

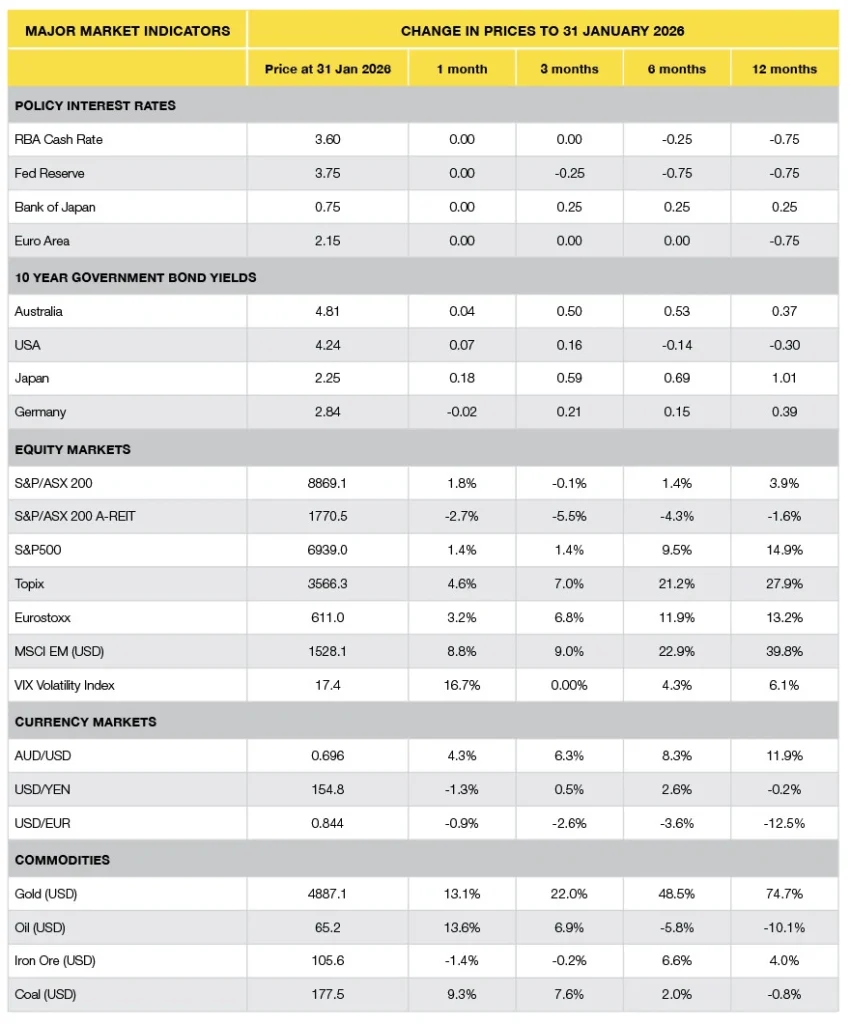

Major Market Indicators

Source: Morningstar, Trading Economics, Reserve Bank of Australia

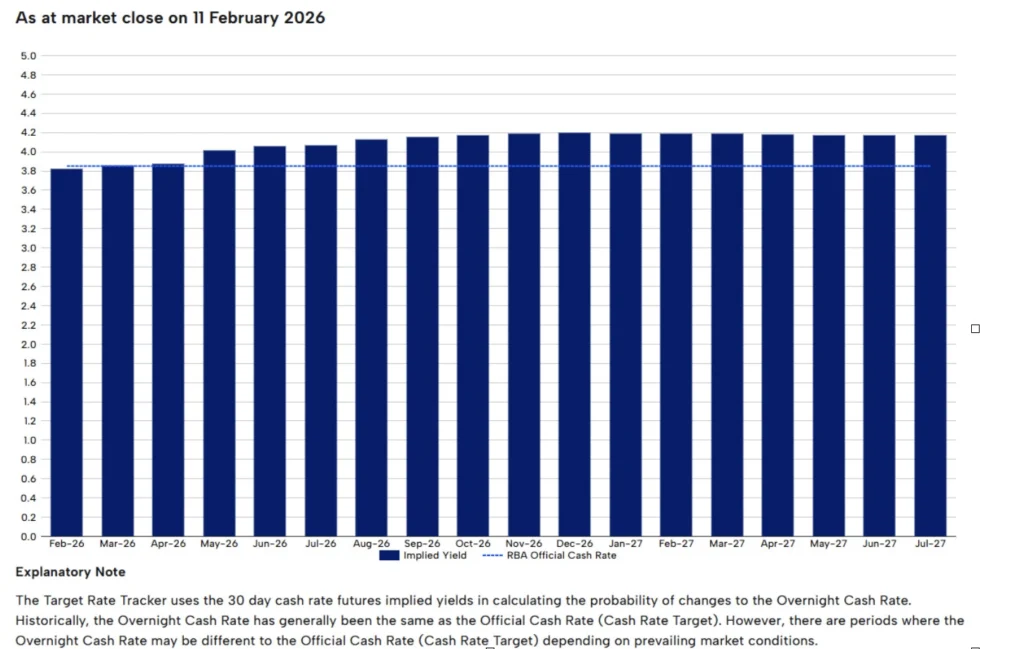

Market Expectations of Future RBA Cash Rates

Expectations are a 4.2% cash rate by end of 2026 …

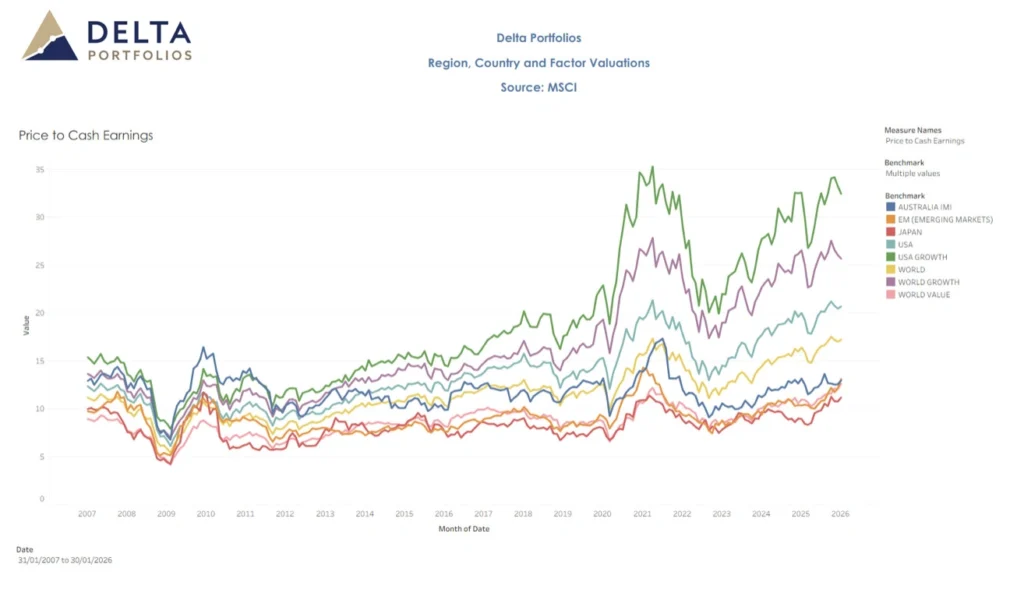

US Growth Valuation Continues Near Double of World Sharemarket Valuations

Published:

Share

Resources

A wealth of knowledge

Latest News

-

Age Pension Assets Test 2026: How Much Can You Have?

July 28, 2026

July 28, 2026

-

Trump Tariffs Australia: What It Means for Your Money

July 28, 2026

-

Financial Planner vs Accountant: Who Helps With What?

July 21, 2026

-

Where Is My Money Going? How to Track Spending In 5 Steps

July 14, 2026

-

Economic Snapshot – June 2026

July 14, 2026

-

Brisbane Property Market: Why Prices Are Holding Firm

July 7, 2026

Tools & Guides

Useful tools & guides to get you started

Video Guides

Useful videos to get you started

Financial Calculators

See what impact little changes can have