Economic Snapshot – Mid-June Market Update 2022

This article was prepared by Michael Furey, Principal of Delta Research & Advisory, on behalf of HPartners Group. IN SUMMARY Higher than expected US inflation has resulted in another market rout. There is an element of it being a little unsurprising as it generally takes many months for higher food and energy prices to filter…

This article was prepared by Michael Furey, Principal of Delta Research & Advisory, on behalf of HPartners Group.

IN SUMMARY

- Higher than expected US inflation has resulted in another market rout. There is an element of it being a little unsurprising as it generally takes many months for higher food and energy prices to filter through. Either way, the Russian/Ukraine war and associated sanctions are not helping (but are necessary and appropriate) as Oil prices continue to increase.

- Recession is factoring into many markets including bonds.

- Either way, the markets outlook is unchanged from a week ago …i.e. for continued market volatility and particularly amongst equity and credit markets, as they are most vulnerable to rising cash rates.

- Taking another step further is the more expensive growth markets (including US Growth, and Tech) are likely to continue their downward price pressures as their valuations continue above long-term trend level.

- Our current preference for portfolio positioning is to avoid concentrated bets (i.e. maintain diversification), rebalance (if not risk averse), and for equity allocations we believe a bias towards cheaper (i.e. Value) securities is preferred. That said, care must be taken to ensure the cheaper securities don’t have balance sheets vulnerable to rate increases, so a Quality bias is also preferred.

- After many years in the investment wilderness, it appears the Value/Quality investment style of Warren Buffett (Age 91) may be back.

- Conservative bonds have declines significantly in price … but current yields appear reasonable value in the face of recession threats

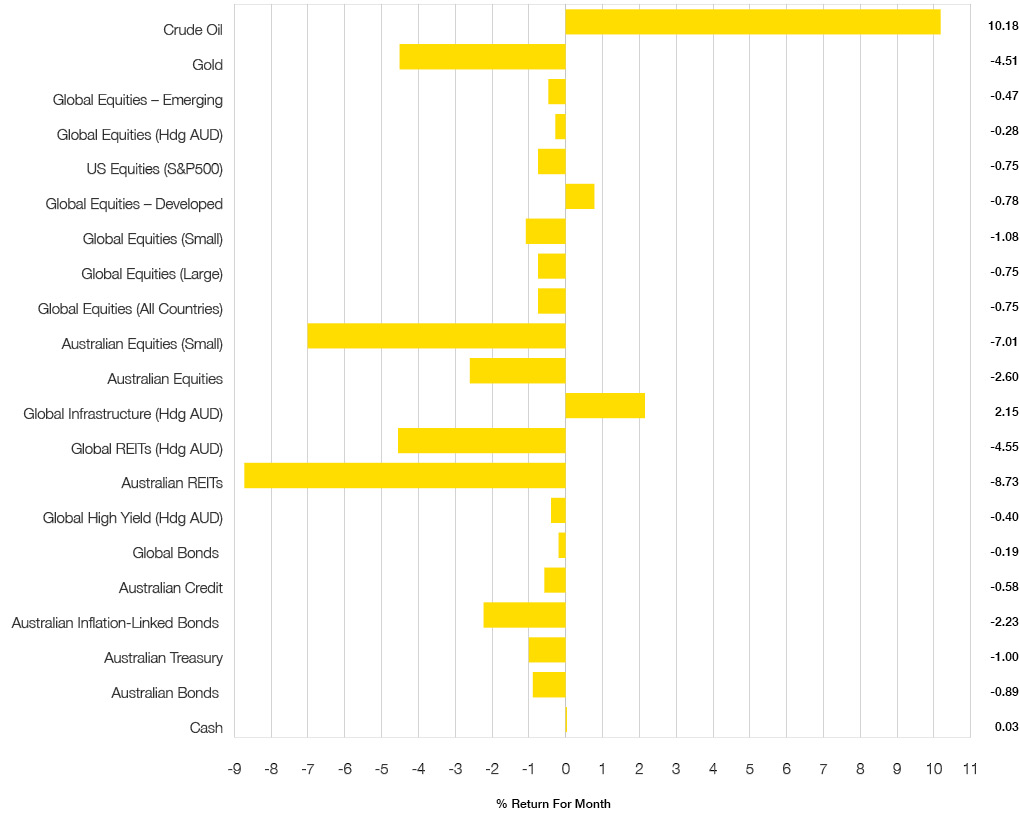

Chart 1: Another difficult month in traditional asset classes

Sources: Morningstar

WHAT HAPPENED IN THE LAST WEEK (TO 14 JUNE 2022)?

Markets & Economy

Volatility is the norm as bond yields soar

- Headline inflation in USA is back to a 40 year high at 8.6% (10 June 2022), Europe’s not far behind (8.1%), Australia’s is over 5%, and our energy prices have come under government control as they threaten to spiral out of control.

- Bond yields around the world have unsurprisingly risen sharply after this high inflation result out of the USA. This means declining bond prices which in turn has resulted in sharp sell-offs by equity markets. Once again, growth markets (e.g. Tech, NASDAQ) appear to have been hit hardest, although pretty much every stock has been sold in the USA and Australia isn’t fairing much better.

- Bond yields are now pointing to US Cash rates hitting 3% in round 12 months, and this will likely mean recession as the higher food, energy, and costs of debts (amongst other price rises) use up everyone’s income.

- Russian/Ukraine war continues without any sign of stopping and Oil prices are now over $120USD per barrel.

- The Australian dollar has declined back below $0.70USD which does help cushion the unhedged global equities allocations, but economically it reduces our overseas purchasing power meaning the cost of goods (in USD) are a little bit higher … including food and energy.

- At this point in time, markets suggest the Reserve Bank is taking interest rates to 3% inside of 12 months, which also suggests runaway inflation locally.

- As a highly indebted nation, that will put a great deal of economic pressure on Australian households and the current economic growth being experienced as we come out of the COVID lockdowns will likely dissipate along with the massive house price increases from which many have benefited.

Outlook

- The following two paragraphs are intentionally unchanged from last month (and the one before)…

- It appears along with inflation, 2022 will likely be seen as a very volatile year for all markets.

- The higher bond yields are resulting in large shifts across equity markets as expensive securities are sold off and the previous momentum of growth, tech, and ESG-friendly themes are replaced by lower valued, lower growth (some may call) boring securities.

- Valuations remain high in USA and still carry downside risks. Whilst Emerging Markets’ valuations continue their appeal, they carry a unique set of risks in the form of China with their continued lockdowns and potential government crackdowns on markets.

- Long term bonds are currently very high and whilst the short-term losses have been painful, this is where the safest returns appear … as any recession could result in lower yields as cash rates increase to combat inflation.

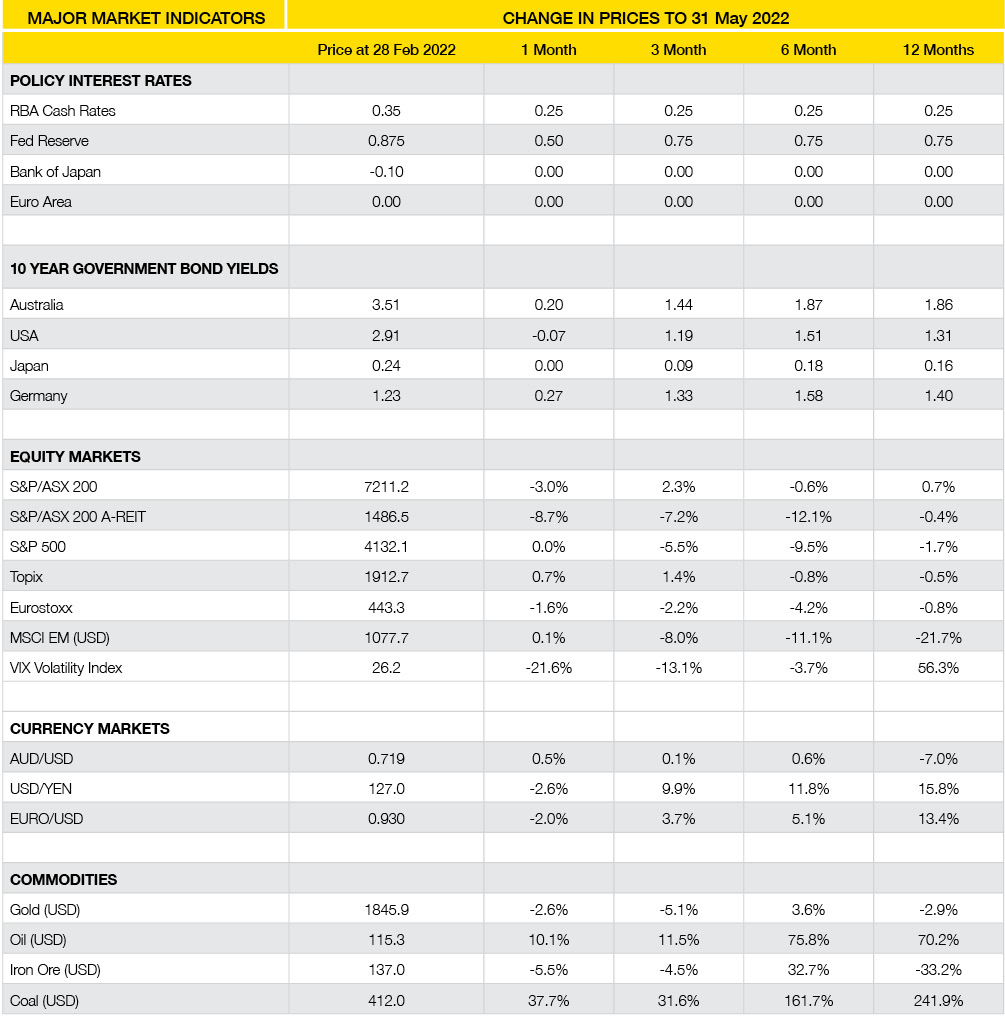

Major Market Indicators

Sources: Tradingview, Morningstar, Trading Economics, Reserve Bank of Australia

Published:

Share

Resources

A wealth of knowledge

Latest News

-

Financial Planner vs Accountant: Who Helps With What?

July 21, 2026

July 21, 2026

-

Where Is My Money Going? How to Track Spending In 5 Steps

July 14, 2026

-

Economic Snapshot – June 2026

July 14, 2026

-

Brisbane Property Market: Why Prices Are Holding Firm

July 7, 2026

-

Splitting Super in a Divorce: What Happens to Your Money?

July 7, 2026

-

Salary Sacrifice 101: Super Support to Boost Your Balance

June 30, 2026

Tools & Guides

Useful tools & guides to get you started

Video Guides

Useful videos to get you started

Financial Calculators

See what impact little changes can have