Economic Snapshot – March 2024

This article was prepared by Michael Furey, Principal of Delta Research & Advisory, on behalf of HPartners Group. IN SUMMARY Happy investors everywhere. Sharemarket momentum continues as Australian, Emerging and Developed markets produce strong returns for a fifth month in a row. Whilst the artificial intelligence theme continues to influence markets as NVIDIA’s strong returns…

This article was prepared by Michael Furey, Principal of Delta Research & Advisory, on behalf of HPartners Group.

IN SUMMARY

Happy investors everywhere.

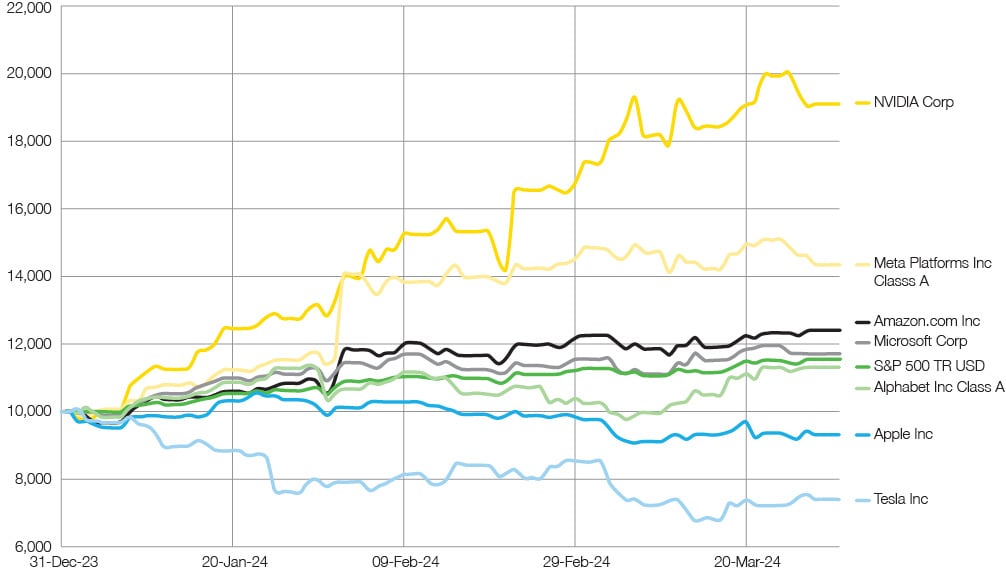

- Sharemarket momentum continues as Australian, Emerging and Developed markets produce strong returns for a fifth month in a row. Whilst the artificial intelligence theme continues to influence markets as NVIDIA’s strong returns continue, several of the so-called Magnificent 7, namely Tesla, Apple and Alphabet (Google), more recently have underperformed the S&P500 suggesting maybe its down to the Magnificent 4 (NVIDIA, Microsoft, Amazon, and Meta).

- Bond markets also produced solid returns as government yields stayed relatively steady but corporate bonds produced capital gains. For March, the investment grade Australian and Global bond markets returned 1.2% and 0.8%, respectively, whilst Global High Yield (AKA Junk Bonds) returned a little under 1.5%

- Slower economic growth appears everywhere except the USA, where its unemployment continues at low levels (3.8%), and the latest economic growth data is the highest in the developed world. Side note … this may be what Biden needs if he is to win the 2024 election as any economic hiccup will likely result in a Trump victory.

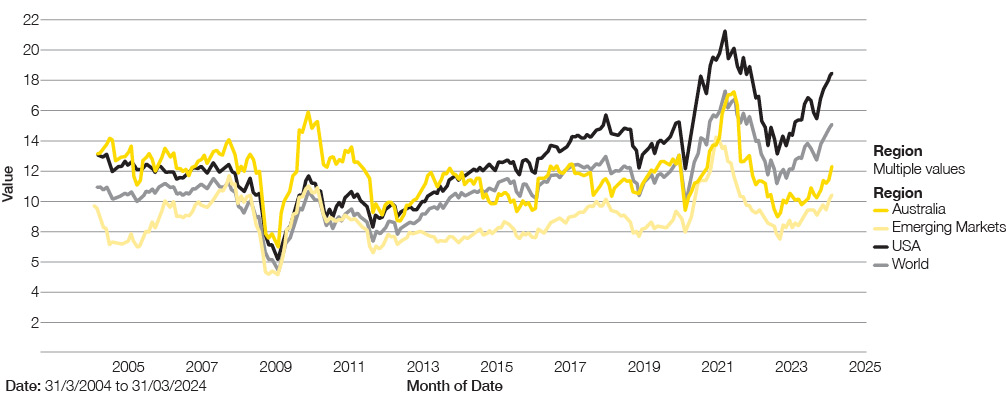

- Otherwise, our message remains the same … valuation is retained as our long-term anchor as it rarely fails over the long term. The US sharemarket has only ever been more expensive around 10% of the time over the last 50 years and the forward returns are not likely to be high. The negative yielding bond market continues as a weaker economy signal.

- So, with both bull and bear market signals everywhere, there are no obvious places to invest, just places to avoid. Emerging Markets and Global Small Companies appear good value, but they still come with significant risks. As a result, portfolio preferences continue to be towards diversification across asset classes and securities.

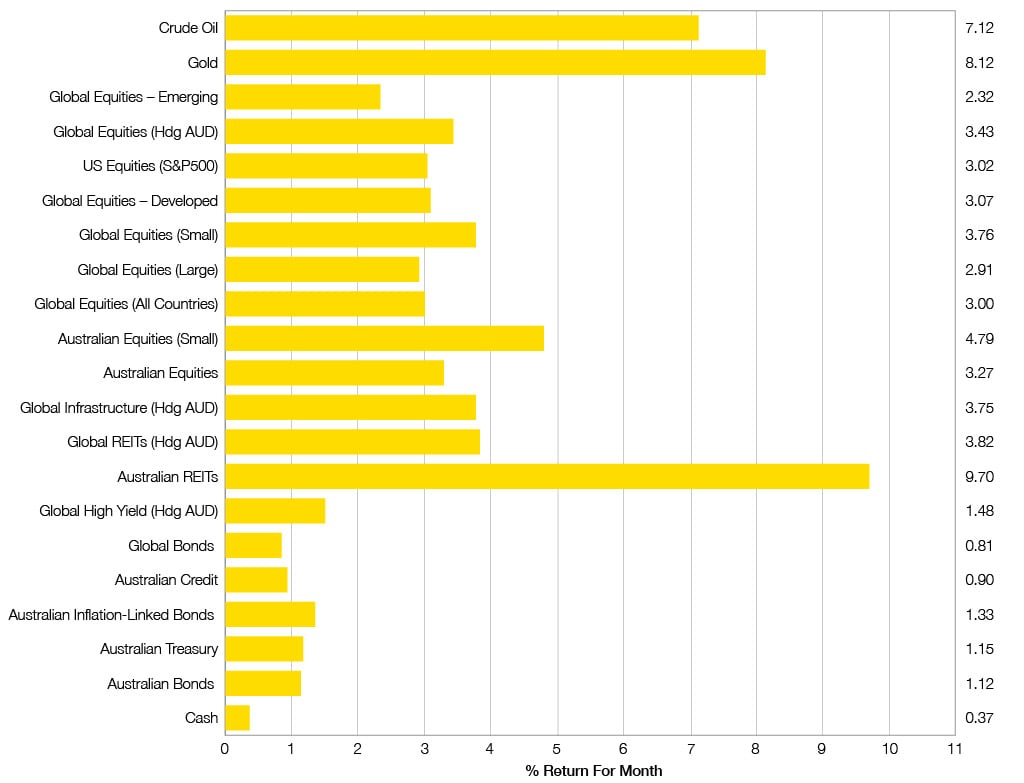

Chart 1: Risk-on momentum continues.

Selected Market Returns in AUD – 31 March 2024

Sources: Morningstar

WHAT HAPPENED LAST MONTH?

Markets & Economy

- It was another strong month all asset class and once again the best performing asset class was Australian REITs. The usual catalyst for strong Australian REIT performance would be lower interest rates but considering they were only down a little bit (well, the 10-year Australian Bond yield to maturity reduced by only 0.13%), we can probably put it down to the overall risk-on environment that appears everywhere and is sometimes referred to as momentum..

- Whilst the artificial intelligence boom continues, the Magnificent 7 has recently reduced to perhaps the Magnificent 4 consisting of Nvidia, Meta, Amazon, and Microsoft. More recent performance has been strong for these shares as Apple, Google, and Tesla have underperformed the S&P500. Please note … these memes rarely last for too long and their persistence is often due to FOMO more than fundamentals.

- The Federal Reserve and the Reserve Bank of Australia continued their rhetoric that the battle of high inflation is not over and at this stage there appears little chance cash rates are declining until the second half of the year. Services inflation and, more recently, some higher food and energy prices, have kept the rate cut agenda on hold for now.

- Unemployment remains very low in the USA at 3.8% and in Australia (3.9%) and this will also keep upward pressure on cash rates and in turn will place downward pressure on sharemarket valuations.

- China, Europe, and now Japan’s economies continue to struggle. China is loosening their monetary policy with lower cash rates and quantitative easing, whilst Europe and Japan have held firm on any monetary policy action, and cash rates are unmoved.

Outlook

There is no change …

- 2024 is generally expected to be a weaker global economy than 2023 however, the USA appears determined to buck this expectation as unemployment continues to be very low and economic growth has surprised on the upsides.

- That said, the US sharemarket is positioned for the opposite of what usually constitutes a long-run bull market. For strong sharemarket returns over the long run, markets are usually valued below long run averages, profit margins are tight, and unemployment relatively high … the reality of today is since 1969, the US sharemarket has only ever been more expensive around 10% of the time, profit margins are high, and unemployment is very low … it feels great as the recent past looks great, but the probabilities are not in favour of strong forward looking returns.

- Bond prices have settled a little over the last few months, and we continue to believe they will most likely provide greater diversification to the sharemarket in 2024 as the focus shifts from inflation to the economy.

- High Yield corporate debt does not appear to provide sufficient return for the risk, and we believe there are better places to achieve higher risk-adjusted returns, so for now our fixed interest preference is investment grade debt.

- With Cash rates yielding higher than bonds, cash continues to be appeal and remains as the fixed interest king.

- Investing with styles that favour value, quality (whether bonds or equities) also appears appropriate but no matter the preferred market, portfolio diversification is crucial.

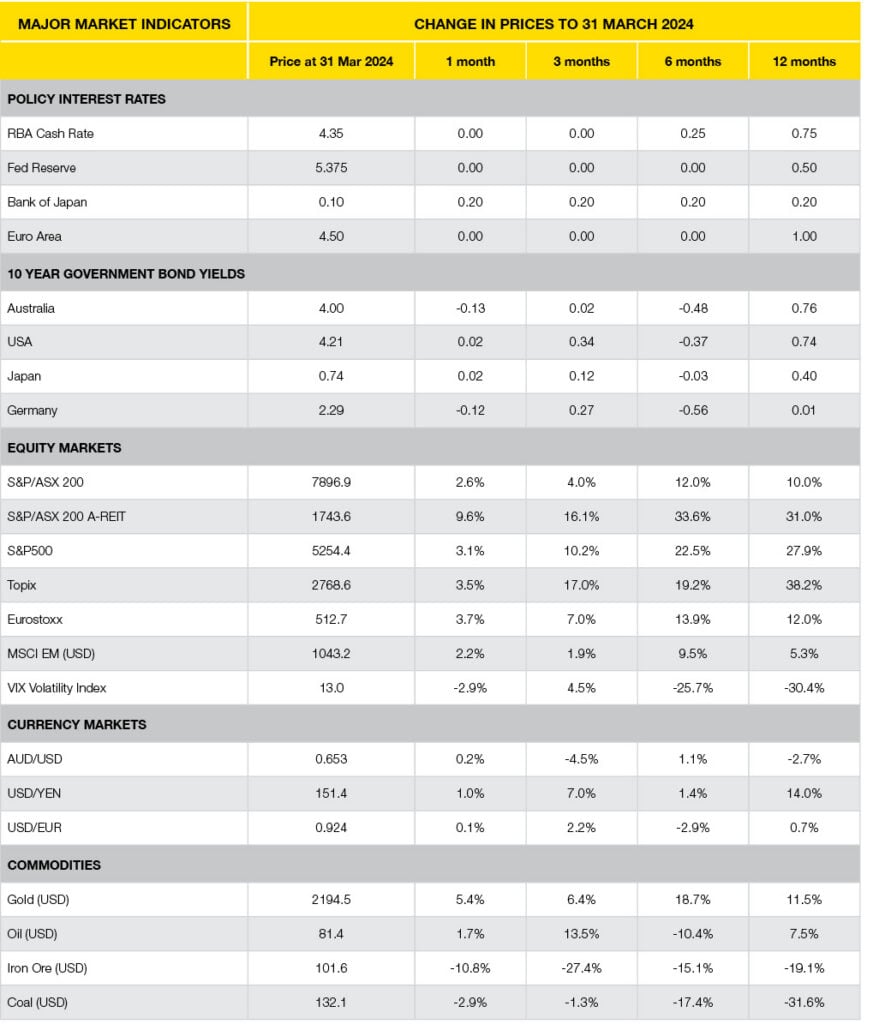

Major Market Indicators

Sources: Tradingview, Morningstar, Trading Economics, Reserve Bank of Australia

Magnificent 7 starts to break up

Performance of Magnificent 7 & S&P500 in 2024

Sources: Michael Read. Source: OECD; Financial Review

Price to Cash Earnings: Regional Comparison – Equity Market Indices

Last 20 Years to 31 March 2024

Sources: MSCI

Published:

Share

Resources

A wealth of knowledge

Latest News

-

Financial Planner vs Accountant: Who Helps With What?

July 21, 2026

July 21, 2026

-

Where Is My Money Going? How to Track Spending In 5 Steps

July 14, 2026

-

Economic Snapshot – June 2026

July 14, 2026

-

Brisbane Property Market: Why Prices Are Holding Firm

July 7, 2026

-

Splitting Super in a Divorce: What Happens to Your Money?

July 7, 2026

-

Salary Sacrifice 101: Super Support to Boost Your Balance

June 30, 2026

Tools & Guides

Useful tools & guides to get you started

Video Guides

Useful videos to get you started

Financial Calculators

See what impact little changes can have