Are Stocks a Good Investment? A Beginner’s Guide

For most Australians aged 20–45 who are new to investing, stocks can be a good investment—but only if you treat them like a long-term project, not a weekend hobby.

In the Australian context, “stocks” usually means ASX-listed shares (often accessed via broad-market ETFs), with returns driven by capital growth + dividends (and, for Australian shares, potentially franking credits). The tax and regulatory rules are manageable, but you do need to understand the basics so you don’t accidentally create a tax mess, overpay fees, or panic-sell at the worst moment.

A practical, beginner-friendly answer to “are stocks a good investment” is:

- Yes, if your timeframe is 5–10+ years, you diversify (often via ETFs), minimise fees, and can tolerate market falls without bailing out.

- Maybe not, if you need the money in the next couple of years, or you’re likely to sell when the market drops. That’s not a moral failing—just a mismatch between the asset and the goal.

Table of Contents

Are Stocks a Good Investment in Australia?

When people ask, “are stocks a good investment?”, they’re usually asking one of two different questions:

First: Do stocks usually grow your wealth over time? Historically, broad share markets have done that—especially when dividends are reinvested—because shares represent ownership in businesses that (on average) grow earnings over time.

Second: Will stocks be “good” for my situation? That depends on your goal timeframe, cash-flow needs, and risk tolerance. Australian consumer guidance commonly groups investments into growth (higher return potential, higher risk: shares and property) versus defensive (lower volatility, lower return: cash and most bonds). Stocks sit firmly in the “growth” bucket.

It also matters which “stocks” you mean:

- Broad-market exposure (e.g., an ETF tracking a big index) behaves very differently from buying a handful of hype-driven small caps. Broad exposure is usually the more sensible starting point for beginners.

- Total return matters. In Australia, dividends are a major contributor to long-term share returns, and many investors reinvest them (e.g., via a dividend reinvestment plan).

Australia’s market is overseen by the national regulator Australian Securities and Investments Commission and operates via the main exchange Australian Securities Exchange, while tax outcomes are governed by the Australian Taxation Office. Those three names show up everywhere in Australian investing for a reason.

Are Stocks a Good Investment? What Australian Market Data Says About Returns and Volatility

If you’re going to invest in stocks, you need two facts in your bones:

- Returns have historically been attractive over long periods.

- The ride is bumpy, and in bad years it can feel like the market is personally offended by your existence.

Long-run returns (Australian shares vs other assets)

A widely used Australian summary (to 30 June 2025) shows Australian shares delivering about 8.0% p.a. over 20 years and about 9.1% p.a. over 10 years (annualised total returns).

That same dataset shows cash and bonds returning materially less over the same horizons (more on that comparison below).

For a more “as-recent-as-possible” snapshot, a large Australian listed investment company publishes benchmark figures to 31 January 2026 showing the S&P/ASX 200 Accumulation Index around 10.2% p.a. over 5 years and 10.1% p.a. over 10 years (annualised), and 7.4% over 1 year in that specific window.

Different end dates produce different “recent” results. That’s normal. It’s also the point: shorter periods bounce around a lot.

Volatility (what you pay for those returns)

Australian equity returns have historically been volatile. A long-run dataset from the central bank Reserve Bank of Australia reports an annual standard deviation for “all shares” around 18.6 (1917–2019), and materially higher volatility for resources-heavy segments.

That doesn’t mean “stocks are bad”. It means stocks are not a savings account. If you might need the money soon, volatility is not a fun personality trait—it’s a practical problem.

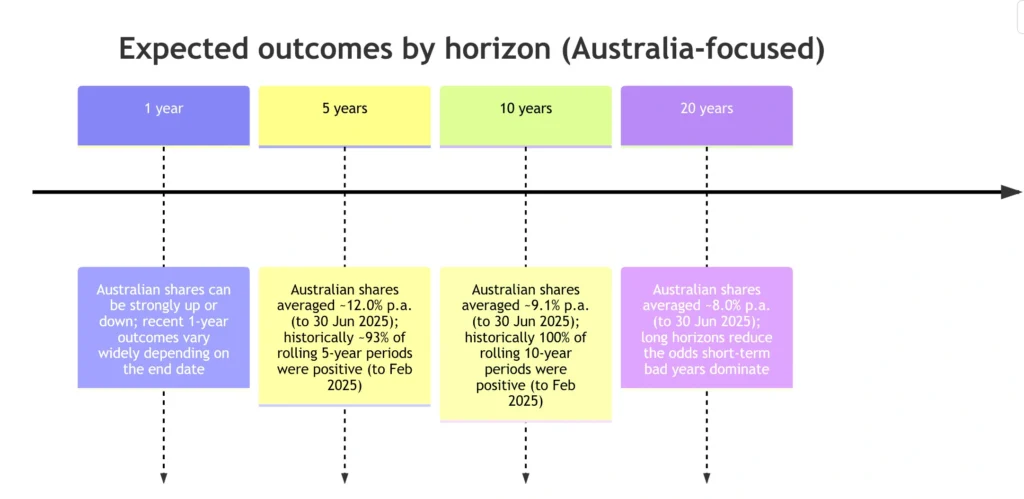

A simple timeline chart: horizon vs return and “risk of loss”

Below is a simple visual to keep expectations realistic. The return figures use Australian shares (annualised total returns to 30 June 2025). The “chance of losing money” is shown using published rolling-period outcomes for the S&P/ASX 200 over its first 25 years (to February 2025).

Are Stocks a Good Investment Compared with Cash, Term Deposits, Property and Superannuation?

This is where the answer gets practical: an investment isn’t “good” in a vacuum. It’s good compared with your alternatives, for your goal.

Asset class comparison table (Australia-focused)

The returns below use long-run Australian data to 30 June 2025 where available. Fees are “typical” ranges a beginner might encounter (they vary by provider).

| Asset class (typical “beginner” version) | Return potential (historical context) | Risk (volatility / loss risk) | Liquidity (how fast you can access cash) | Typical fees & costs (Australia) |

|---|---|---|---|---|

| Stocks (Australian shares via broad ETF) | ~8.0% p.a. (20y), ~9.1% p.a. (10y) to 30 Jun 2025 | High; equity volatility has historically been substantial | High (sell on market; cash after settlement) | Brokerage per trade (online brokerage “starting at around $20”); ETF has ongoing management fee (typically lower than managed funds) |

| Cash / bank bills (proxy for savings-type returns) | ~3.4% p.a. (20y), ~2.0% p.a. (10y) to 30 Jun 2025 | Low | Very high | Usually no explicit investment fee; “cost” is inflation risk (purchasing power) |

| Term deposits | Varies with interest rates; designed for certainty rather than maximising returns | Low (but inflation risk remains) | Medium (funds locked for a term; early break conditions vary) | Generally no management fee; opportunity cost and possible break costs; fixed rate interest |

| Australian bonds (broad index exposure) | ~4.3% p.a. (20y), ~2.3% p.a. (10y) to 30 Jun 2025 | Low–medium (interest rate sensitivity) | Medium–high (depends on product) | Fund/ETF management fee + trading costs; typically lower volatility than shares |

| Listed property (A-REIT index exposure) | ~5.4% p.a. (20y), ~8.3% p.a. (10y) to 30 Jun 2025 | Medium–high (market-traded; can fall sharply) | High (traded like shares) | Brokerage + ETF/fund fee; property sector concentration risk |

| Residential property (direct investment) | Long-run house price growth has differed by era; RBA cites ~7.2% p.a. nominal (1990s–mid 2000s) and “a little over 5%” nominal in the decade prior to 2015 | Medium (prices can fall; leverage amplifies outcomes) | Low (selling takes time; high transaction costs) | High one-off costs (stamp duty, legal, agents), ongoing costs; rental deductions rules are detailed |

| Superannuation (diversified option) | Often a mix of shares, bonds, property; long-term returns depend on allocation | Varies by option (balanced vs high growth etc) | Low until conditions of release; designed for retirement | Admin + investment fees; tax treatment differs from personal investing |

So, are stocks a good investment “versus” these alternatives?

- Versus cash/term deposits: Stocks have historically offered higher long-run returns, but cash products win on stability and short-term certainty. Cash is where your emergency fund belongs; stocks are where your long-term wealth-building can happen.

- Versus property: Property can build wealth, but it’s not automatically safer—especially once you include leverage and illiquidity. Residential property also has significant frictional costs and complexity compared with buying a diversified ETF.

- Versus superannuation: For many Australians, the most under-rated move is simply getting super right first (fees, investment option, contributions strategy). Note that super is often already heavily invested in shares; you may already be an investor, whether you realise it or not.

Pros and Cons of Stocks for Australians Aged 20–45

The case for stocks being a good investment

Stocks can be a good investment because they offer:

Higher long-term return potential than cash and bonds, historically, especially when viewed over decades rather than months.

Liquidity and flexibility: you can usually buy/sell easily through an online broker and scale up contributions over time.

Access to diversification at low cost when you use broad ETFs (effectively buying a basket of shares). This is especially useful when you’re starting with smaller amounts.

Australian-specific dividend features: Australian shares often pay dividends, and the tax system includes franking credits in many cases, which can materially affect after-tax outcomes depending on your situation.

The case against stocks (or: when they’re a bad match)

Stocks can be a poor choice if:

Your timeframe is short (e.g., saving for a home deposit you’ll need soon). Shares can fall sharply and stay down long enough to ruin your plan.

You can’t tolerate volatility. If a 20% fall will cause you to sell in a panic, the “expected return” you’ll actually experience can be far lower than the market’s. Volatility is as much behavioural as mathematical.

You concentrate risk (a few stocks, one sector, one theme), or you treat investing like entertainment. The market will happily accept your donation.

You ignore fees and taxes. Brokerage, ongoing fund fees, and tax outcomes can be the difference between “this is working” and “why am I doing this?”

Risk Management: How to Make Stocks a Good Investment in Practice

If you’re trying to make the answer to “are stocks a good investment” a confident “yes” for your own life, risk management is the whole game.

Diversification first, cleverness second

Diversification reduces portfolio risk and can make returns more stable. That means spreading across companies, sectors, and (often) geographies—rather than betting your future on a handful of names.

For beginners, diversification is often easiest through:

- ETFs that track a share index (e.g., a broad Australian equity ETF)

- Managed funds (often higher ongoing fees than ETFs, depending on the product)

Blue-chips vs small caps: what matters for beginners

A simple frame that helps:

- Blue-chip / large established companies: usually more widely researched, often more liquid, and may feel “steadier” (still not guaranteed).

- Small caps: can grow faster, but usually with more volatility and business risk.

The beginner mistake is thinking “small” automatically means “more upside” without acknowledging the higher probability of permanent loss. Diversification is how you take part in growth without needing perfect stock-picking skills.

Dividends, reinvestment, and compounding

Reinvesting dividends (and distributions) can materially increase long-term outcomes because it harnesses compounding. Some dividend reinvestment plans are easy to set up and may avoid brokerage costs, but you generally give up control of the purchase price.

Crucially, reinvesting does not make the dividend “tax-free”; you still generally declare it as income (details below).

Practical Steps to Start Investing

This is the part where you move from “thinking about investing” to “actually doing it”.

Choose your route: direct shares vs funds/ETFs

In Australia, a common beginner pathway is:

- Start with a diversified ETF (broad market)

- Add individual companies later if you genuinely want to research them

This approach reduces the risk of building a “portfolio” that is secretly just three bank stocks and a mining stock you bought because your mate’s uncle “has a feeling.”

Pick a broker and understand fees

The most common way to buy and sell shares is via an online broking service (you do your own decisions) or a full-service broker (they trade and may advise, with higher cost structures).

Cost examples from Australian consumer guidance include:

- Online brokers: you pay a fee each time you buy/sell – starting at around $20 per trade (varies).

- Full-service brokers: fees are typically a percentage of trade value, with minimums; small trades can be relatively expensive.

Also, be alert to fraud: consumer guidance notes reports of stolen shares due to identity theft and links to investor alerts. In plain English: use strong passwords, protect your ID, and don’t treat account security as optional.

Decide your account type and ownership structure

Beginners commonly invest via an individual account or joint account; more complex structures (trust/company) can make sense in specific circumstances but add complexity.

If you invest indirectly (ETFs/managed funds) you’re often buying units rather than holding the underlying shares directly. Some structures (like depositary arrangements for certain international exposures) mean legal title is held by a nominee on your behalf. Make sure you understand what you’re signing up for.

If fractional shares matter to you, treat it as a feature to verify—not an assumption. Availability and ownership mechanics depend on the platform and the asset. (No, you can’t just assume “fractional” works the same everywhere. Investing loves fine print.)

Understand franking credits and DRPs before you tick the box

Two Australia-specific features that beginners run into quickly:

- Franking credits: Depending on your circumstances and eligibility, you may be entitled to a franking credits tax offset and potentially a refund (subject to integrity rules and other conditions).

- Dividend reinvestment plans (DRPs): You generally still declare the dividend as income even if it’s reinvested, and the additional shares acquired become relevant for CGT calculations later.

Tax Basics, Common Mistakes and The Starter Checklist

Australian tax basics for share investors

For most beginner investors (not running a share-trading business), the common tax touchpoints are:

Dividends and franking: When you own shares, there are tax implications from receiving dividends and franking credits.

Capital gains tax: CGT commonly applies when you dispose of shares (sell, or certain other events).

CGT discount: If you’re an Australian resident individual and you hold an asset for at least 12 months before the CGT event, you may be eligible for the CGT discount (often 50% for individuals, subject to the rules).

Record-keeping: The tax office is explicit about keeping records so you can identify which shares you sold, acquisition dates, and cost base details. If you don’t track it, future-you will pay for present-you’s laziness—possibly with interest, and definitely with vibes.

Common beginner mistakes (and how to avoid them)

Mistake: investing money you’ll need soon. Fix it by matching timeframe to asset class: short-term goals usually need lower volatility options.

Mistake: underestimating diversification. Fix it by starting with broad ETFs or diversified funds rather than a tiny handful of shares.

Mistake: ignoring fees. Fix it by understanding brokerage per trade and ongoing product fees, and by avoiding constant tinkering that generates costs.

Mistake: forgetting tax until June. Fix it by keeping records as you go, and understanding dividends/DRP/CGT basics early.

Mistake: panic-selling. Fix it by having a written plan (goal, timeframe, contribution plan, and rules for when you’ll rebalance or review). The Australian Securities Exchange investor education material explicitly frames investing time horizons and portfolio review as part of an investment plan.

Starter checklist

- Set the goal and timeframe (be specific: “home deposit in 2 years” vs “retirement in 30 years”).

- Build an emergency buffer first (stocks are not your emergency fund).

- Start diversified (often a broad-market ETF) and keep contributions regular.

- Minimise avoidable costs (brokerage, unnecessary trading, high ongoing fees).

- Get your tax basics right from day one (dividends, franking credits, CGT discount, and record-keeping).

Conclusion: Are Stocks a Good Investment?

For Australians who are new to investment planning, stocks are often a good investment when you use them for what they’re good at: long-term growth. The historical data shows strong long-run returns for Australian shares relative to cash and bonds, but also meaningful volatility that makes short-term investing risky.

So the honest answer is:

- Yes—stocks can be a good investment if your horizon is long (think 5–10+ years), you diversify (often via ETFs), and you can stay invested through market falls.

- No—stocks are not a good investment for money you need soon, or if you’re likely to bail out during volatility. That’s not pessimism; that’s matching the tool to the job.

Any advice is general in nature only and has been prepared without considering your needs, objectives or financial situation. Before acting on it, you should consider its appropriateness for you, having regard to those factors. Before making any decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement.

Published:

Share

Resources

A wealth of knowledge

Latest News

-

Age Pension Assets Test 2026: How Much Can You Have?

July 28, 2026

July 28, 2026

-

Trump Tariffs Australia: What It Means for Your Money

July 28, 2026

-

Financial Planner vs Accountant: Who Helps With What?

July 21, 2026

-

Where Is My Money Going? How to Track Spending In 5 Steps

July 14, 2026

-

Economic Snapshot – June 2026

July 14, 2026

-

Brisbane Property Market: Why Prices Are Holding Firm

July 7, 2026

Tools & Guides

Useful tools & guides to get you started

Video Guides

Useful videos to get you started

Financial Calculators

See what impact little changes can have